03 Feb Maximizing Wealth Accumulation with Life Insurance: A Comprehensive Guide to Securing Your Financial Future

Wealth Accumulation with Life Insurance

In today’s dynamic financial landscape, individuals and families are seeking comprehensive solutions to secure their financial future and achieve their long-term goals. In this comprehensive guide, we explore the powerful intersection of life insurance and wealth accumulation strategies. From understanding the nuances of different life insurance policies to leveraging tax advantages and planning for retirement and estate distribution, this guide aims to equip you with the knowledge and insights needed to make informed decisions about your financial well-being.

Key Sections:

-

Understanding Life Insurance:

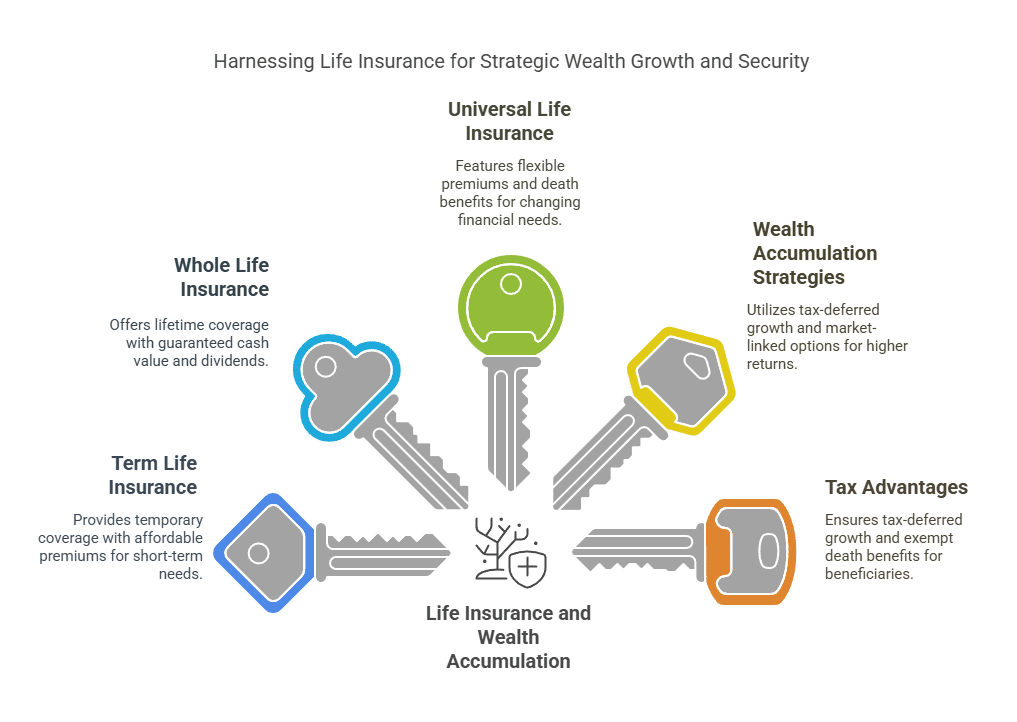

- Term Life Insurance: Term life insurance provides coverage for a specified period, typically 10, 20, or 30 years. It offers affordable premiums and straightforward coverage, making it an ideal choice for individuals with temporary insurance needs, such as young families or individuals with outstanding loans.

- Whole Life Insurance: Whole life insurance offers lifetime coverage with guaranteed premiums and a cash value component that accumulates over time. It provides permanent protection and cash value growth, making it suitable for individuals seeking long-term financial security and asset accumulation.

- Universal Life Insurance: Universal life insurance offers flexibility in premium payments and death benefit options. It allows policyholders to adjust their coverage and premiums according to their changing financial needs and offers potential cash value accumulation based on current interest rates.

-

Wealth Accumulation Strategies:

- Life insurance policies serve as effective wealth accumulation tools due to their cash value component. Cash value accumulates on a tax-deferred basis, allowing policyholders to grow their wealth more efficiently compared to taxable investment accounts.

- Indexed universal life (IUL) policies offer the potential for higher returns by linking cash value growth to the performance of a stock market index, such as the S&P 500. Policyholders can benefit from market gains while being protected from market downturns.

- Whole life insurance policies provide guaranteed cash value growth and dividend payments, offering stability and predictability in wealth accumulation. Policyholders can access cash value through policy loans or withdrawals to supplement their income or fund major expenses.

-

Tax Advantages of Life Insurance:

- Life insurance policies offer several tax advantages that can enhance your overall financial plan. The cash value component grows on a tax-deferred basis, meaning you won’t pay taxes on investment earnings until you withdraw funds from the policy.

- Death benefits paid to beneficiaries are typically income tax-free, providing a tax-efficient way to transfer wealth to heirs. Additionally, life insurance proceeds are generally exempt from probate, ensuring a swift and private distribution of assets to beneficiaries.

- Certain life insurance policies, such as indexed universal life (IUL) policies, offer potential estate tax advantages by providing liquidity to cover estate taxes and ensuring heirs receive their inheritance without the burden of tax liabilities.

-

Retirement and Estate Planning:

- Life insurance plays a vital role in retirement planning by providing income replacement for surviving spouses and dependents. With the death benefit proceeds, beneficiaries can maintain their standard of living and cover essential expenses in retirement.

- Additionally, life insurance can be used as a strategic estate planning tool to provide liquidity for estate taxes and ensure a smooth transfer of assets to heirs. Irrevocable life insurance trusts (ILITs) are commonly used to hold life insurance policies outside of the estate, reducing potential estate tax liabilities and preserving the value of the estate for future generations.

-

Family Protection and Financial Security:

- At its core, life insurance offers peace of mind and financial security for your loved ones. In the event of your passing, life insurance provides income replacement to cover living expenses, mortgage payments, and other financial obligations.

- Life insurance proceeds can also be used to pay off debts, such as credit card balances, student loans, and outstanding mortgages, relieving financial burdens on surviving family members.

- Furthermore, life insurance can fund future expenses, such as college tuition for children or grandchildren, ensuring they have access to quality education and opportunities for success.

Conclusion:

Life insurance is a versatile and powerful tool for securing your financial future and maximizing wealth accumulation. By understanding the different types of life insurance policies, their tax advantages, and their role in retirement and estate planning, you can take proactive steps to protect your family, preserve your assets, and achieve your long-term financial goals. Contact The Policy Shop today to explore your life insurance options and embark on the journey to financial security and prosperity.

________________________________________________________________________________________________________________________________________________

- Secure Your Future with The Policy Shop

Explore our comprehensive life insurance solutions designed to fit your financial goals and protect your loved ones. Whether you’re planning for retirement, safeguarding your family’s future, or exploring innovative insurance strategies, The Policy Shop is your trusted partner in financial security.

Ready to take the next step? Contact our expert advisors to discuss your insurance needs and find the perfect policy.

Subscribe to our newsletter for the latest insights on life insurance, financial planning tips, and exclusive updates from The Policy Shop.